Bonds

Jan 15, 2017

If you would prefer to listen to me read this blog post, please click on the play button.

Yippee and welcome to 2017. Happy New Year!

I have been spoiled for choice with blog ideas but I’ve decided NOT to follow the general media who in January are always focused on debt repayment after the Christmas spend up, goal setting for the coming year and how to save for ‘must haves’ like a new sofa. For the record a new sofa is NOT an investment.

Saving is a steady ship where I am looking at a long term journey so let’s not get too excited about things just because a new year has started!

So the plan is, I’m going to continue on just as I was before, focussing on investing, looking at ways to invest and thinking about new things to invest in. Fabulous subscribers have emailed me all sorts of things they want to know more about and one of them is BONDS. This topic has been on my radar for a while but quite frankly I am starting from a knowledge base of “stuff all” as I’ve never really considered buying bonds so as a result have never sought out any information on them. It turns out they are a relatively simple concept but have exposed me to the world of debt markets, something I’ve been actively trying to avoid.

A Bond (also called a debenture) is a loan you make to a government, state owned enterprise, council or company. Perhaps they have a specific project they are working on and they need to raise some cash to do it. The NZ Government has “Earthquake Bonds” to help them cover the costs of the Christchurch rebuild and other quake damage for example. You agree to loan them some of your cash for a specific time frame and for a specific return by way of an interest payment (also called a coupon rate). At the end of the agreed period you get your lump sum back as well as all the interest paid out over the period of the bond.

Eg: In 2017 you invest $10,000 at 6% coupon rate (interest paid biannually). Maturity date 2023.

You can also buy a perpetual bond that never matures but keeps pumping out a steady income of fixed interest amounts to you for years to come IF the company continues to perform well.

Unlike a term deposit I can sell them at any time on the HUGE bond market and there appears to always be a willing buyer for good bonds. BUT the price of that bond can change dependent on whether people want to buy that bond... or not.

Bonds are a ‘liquidity risk’ - there might not be a buyer when we want to sell. Furthermore that company might fail during the life of the bond and I might never get paid.

Why is investing never straight forward? Why will there always be people happy to borrow my money but are vague about whether I will get it back?

Another risk is that they are unlikely to keep up with inflation. If you invest $10,000 in a perpetual bond (i.e. forever), yes you will get interest paid out regularly but your lump sum will be worth less over time. $10K was a decent chunk of change back in 1987 but not so today.

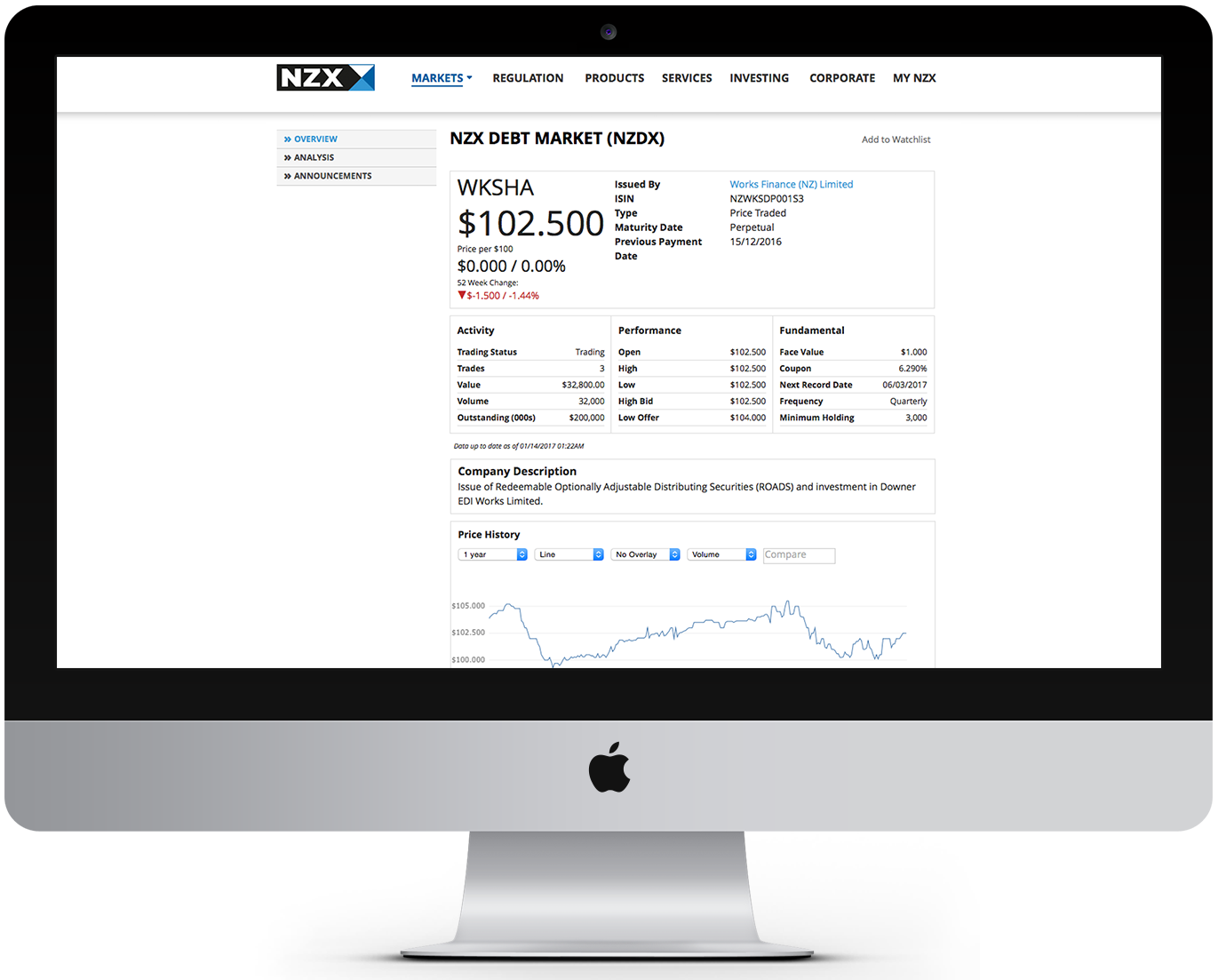

For obvious reasons I have always avoided anything to do with debt so had never even looked at the debt market on the NZX. Did you realise that when you go on the NZX website there are more exciting markets you can look at, additional to what you see on the home screen? If you click on the “markets” tab you can select the NZX Debt Market.

This is where you will find bonds listed.

The debt industry is beyond massive. Companies find lending off banks far too restrictive. Think of your own mortgage and all the rules that apply to that and times that by 100 if you were a company. So, instead they turn to bonds to get the cash they need from hundreds or thousands of investors to grow their business or industry. Yes, they could issue shares, but in doing so they are giving up ownership of the company bit by bit. Bonds offer them freedom to do as they choose with that money and the investor has clarity about their returns too. They know how much they are lending, over what term and for a set coupon rate. It’s like everybody kicked a goal!

Here is an example of a bond on the NZX debt market for “Works Finance (NZ) Limited. A wholly owned subsidiary of Downer EDI Limited and was formed for the purpose of issuing ROADS”.

Nope, I had never heard of them either!

Picking a bond to invest in carries a similar warning as picking a share and that is to only invest in what you know and understand. When I take a poke around the NZX Debt market it is full of ticker codes that I don’t recognise so I would really need to do my homework if I wanted to get involved. Some ticker codes I found for companies raising money to run their businesses:

CASHA - I read the Analysis on them and still don’t know what they do

GPLFA - Genesis Energy

RCSHA - Rabobank Group is an international financial service provider

WTF - OK, I made that one up to see if you were paying attention

You can buy and sell bonds just like shares and like shares the price can rise and fall and the bank savings and interest rates on offer really affect what your bond might be worth. If bank interest rates have risen then the buyer will want to pay you less for it.

Say your bank was offering an 8% return on the $10,000 you invested with them but you could buy a bond offering a 10% return or coupon rate. The bond is a better buy right?

But if in two years time your bank is offering a 12% return (hahahaha) then suddenly (or slowly) your bond with a 10% return is not looking quite so rosy or desirable. You could still sell it but people will offer you less than what you paid. On the other hand if interest rates at your bank dropped your bond is looking like a good buy and people will be willing to pay you more to get that higher return.

How can I assess risk to help pick a goodie?

You can find out the risk level of your bond by looking at its rating. You have heard of Standard and Poor’s ratings right (or Moody’s or Fitch)? AAA and all that? Just to fill you with confidence they get rated according to how unlikely they are to default, from the top AAA (top notch bond) right down to D (run a mile bond). Not all bonds are rated (they may be too small) but the higher the rating and the more likely it is you will get paid. Anything with a credit rating of BBB minus or better are considered ‘investment grade bonds’. Anything lower than that is possibly an indication that the company is experiencing some drama and need the cash. This might be a sign of doom or it might be that they use that money to turn things around and you will be paid. Because they are riskier the interest rates they pay are often much higher.

I didn’t want to get too bogged down today but one other note was the different types of bonds that can give you some added security. If you have bought “senior bonds” and a company fails you can be first in line for grabbing the leftover scraps. If you have purchased “subordinated bonds” you will be in line to get the crumbs left over once they have dealt with the scraps. Government bonds are guaranteed but corporate and local authority bonds are not.

Well, after ploughing through lots of websites, several books and a few podcasts should I buy some? It turns out I already have. Chances are if you are part of KiwiSaver you already have too. When I look at the fund I’m in for KiwiSaver it has “fixed interest” investments which make up a small percentage of my fund. These are bonds.

If you are still confused as to why you might buy a bond when they typically have a low interest rate/coupon rate and often a lower return over time, it is all about diversification. They can provide a low risk investment with a steady income and you can sell them if you suddenly decide to book a cruise to Jamaica. But thinking back to the minefield of buying individual shares and how to pick a winner I think my best bet would be to buy into a fund with a range of bonds, which appears to be what I have already done via KiwiSaver! Here is an example of a Fund made up of Bonds: www.ampcapital.co.nz

From everything I have read I’m alarmed at the amount of references to the company failing and losing all of my money! But the fact remains that bonds are a massive massive market and clearly people are making money. In my mind the debt market gets pretty convoluted pretty quickly and I would have to do a lot more research to get my head around who is selling bonds, why they want to sell them and is the return worth it for me. Now that I feel more schooled up on them they are definitely on my radar though and I’m going to investigate further. If I needed to put some money somewhere for a shorter length of time then some low risk, short term bonds could work. They won’t make as much money as some other investments but I am very likely to get all of my money back at the end and earn a set amount of interest at the same time.

I will let you know if I invest.