Our Coast FI Plan: Keep the House, Invest Less

10 May, 2026

OK. Where to begin.

Jonny is 53, and I’m 52. And if I’m honest, I’m a little annoyed at myself that we are not fully work optional. We are absolutely getting there - dangerously close, I’d say - but not quite there, yet. We have a huge amount of autonomy over our time, which I don’t take for granted for a second, but I still wouldn’t call us fully work-optional.

If you include our paid-off house, we have the net worth to retire now ($1,750,000), but it’s in the wrong places to provide an income: too much house (around $1,000,000), and too few shares (around $750,000). And to retire early, you need assets (shares) that generate income. Our $750,000 investments do, just not quite enough yet.

If you are new here, what on earth am I on about?

There are two rough calculations you can do to determine how financially independent you are. For example:

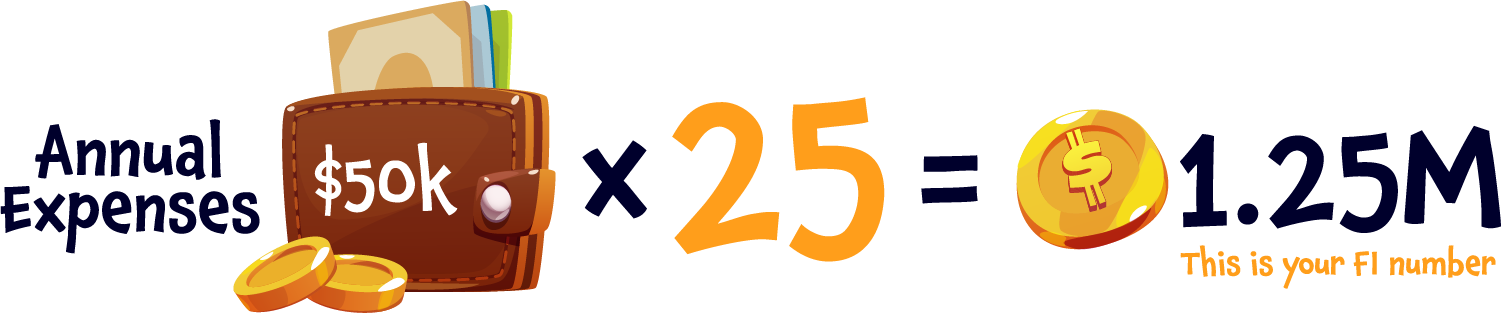

Annual Expenses $50,000 x 25 = $1,250,000 (this is your FI number)

When your investments reach $1,250,000, you can sell off 4% per year, giving you $50,000 to cover your expenses.

Still work… just less of it

Jonny is currently working two days a week as a graphic designer, and given the gentle growth of The Happy Saver, I’ve essentially ended up working for myself. It’s a slightly odd ‘job’ I’ve created, given that 90% of what I do is done for free, but it has grown to the point where it provides a good income with very favourable working hours. The work feels useful and meaningful, and I have a lot of freedom as to how I spend my time, which is glorious.

But it’s still work. My inbox is forever calling me.

Jonny is just about done with the whole concept of work. He wants to quit, and I fully support him. He wants a change of pace, which doesn’t seem unusual at all at this stage of life. Thankfully, that absolutely includes continuing to work with me on The Happy Saver, which we both genuinely enjoy.

The fork in the road

So, here we reached a bit of a tipping point.

We found ourselves at a T-intersection, and we could go left or right. We could keep the status quo, where Jonny keeps working, we keep investing, and we grow our income-producing share assets until we reach our FI number of around $1.2 million invested. Or we could take a more decisive step and downsize our house, invest the surplus, and effectively fast-track things, meaning that Jonny quits, we travel more, and we both continue working on The Happy Saver.

We had more or less picked option two. It seemed logical. Sell the house, buy a cheaper one, invest the difference, and move on with life.

Easy peasy. However, math butts up against emotion, and nothing is black and white once you dig into it.

Why selling didn’t sit right after all

I thought I was very much on board with selling the house. I’ve moved many times over the years and have great memories of most of those homes, so I figured this one would simply become another good memory. But the more I sat with it, the more I realised that this move didn’t feel quite the same. In the past, moving felt like we were going towards something better. This time, it felt like we’d be moving into a house, with the price being the primary deciding factor, and that didn’t feel particularly exciting.

More than that, I could see the next 12 months stretching out before us, filled with selling, buying, and mucking about with setting up a new house. And I realised I’m just not interested in that. And I’m not interested in doing DIY anymore. I want the next year to be about living life, not managing a property transaction and all the work that comes with it.

So, something felt off.

Interestingly, we both took turns being the one pushing for the sale. Initially, it was me convincing Jonny that it made sense. Then I got cold feet, and Jonny was the one pushing to go ahead. So we talked about it, again and again, and we also reached out to friends in the FI community whose opinions we really value.

We are so fortunate to have a wide range of friends who are living out their version of FI. Some own houses, some don’t. Some work, some don’t. All of them are investors, and those investments pay them an annual income.

We mulled over all our options, and eventually, things became clearer.

The third option that changed everything

We realised there was a third option.

We knew we were already “Coast Financial Independence”. So we took a deeper look.

Coast FI simply means that if we never invest another cent into our InvestNow KiwiSaver Foundation Series Total World Fund or our Smart Total World Fund ETF, those share market investments will continue to grow and compound on their own.

How? We own so many shares now that, for example, a share we bought for $2 in 2016 is now worth $5. As each share goes up in value (a capital gain), our total balance grows.

Given our current investment balance and assuming a fairly typical long-term return of 8%-10%, we will reach our full FI number in a few short years.

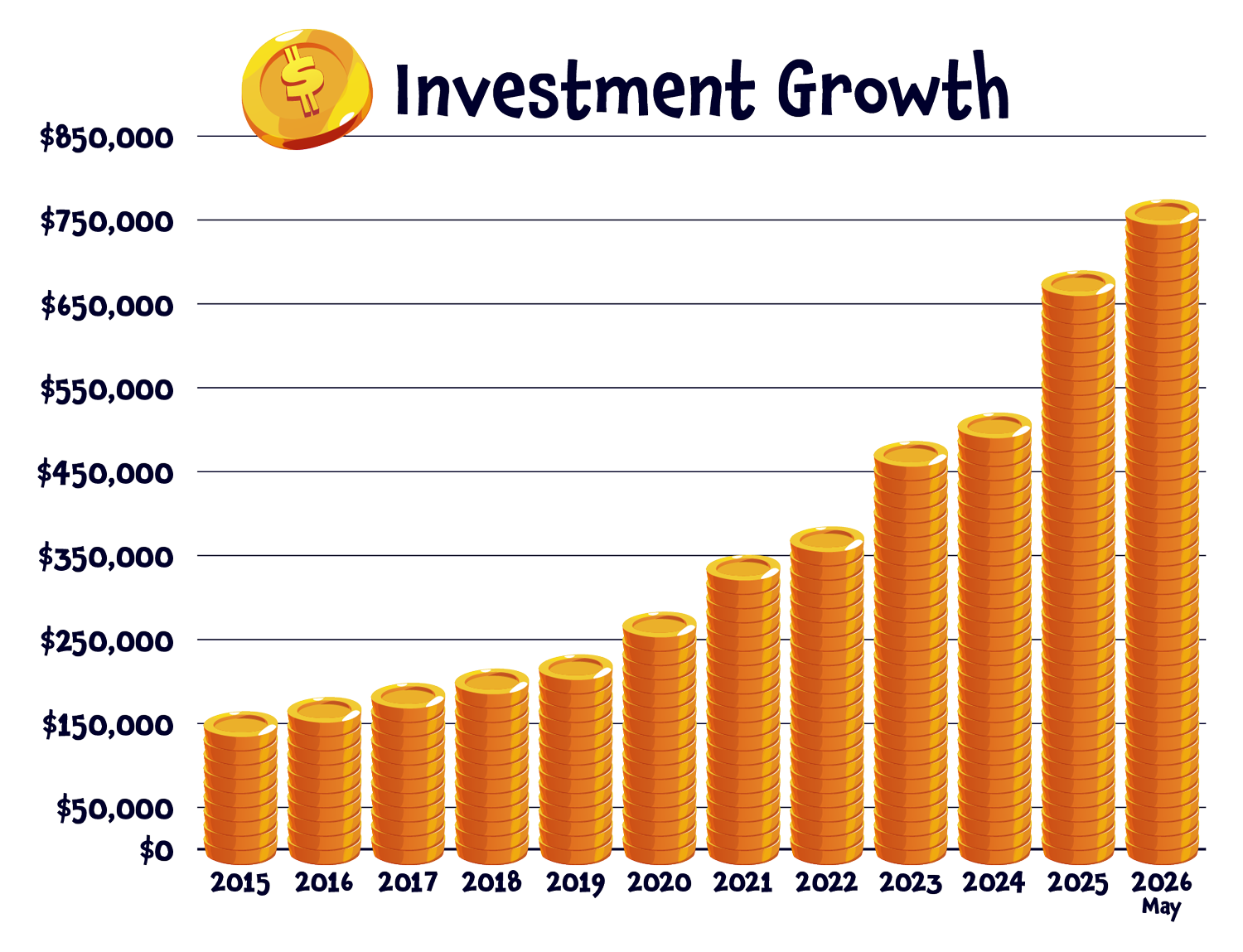

Our investment growth over the last decade.

Meaning that instead of pushing hard to invest as much as we can to accelerate things, we can ease off on how much we invest, and let ‘time in the market’ do more of the work.

Once we saw that, many other decisions fell into place.

What we’re actually doing now

We are going to keep our house. One of the most helpful questions we were asked was: if we had $1,000,000 in cash, would we buy this house? And somewhat surprisingly, the answer was yes. The main reason for selling was financial - we estimated we could free up around $300,000 to invest - but our investments are on track to grow by a similar amount within a few years anyway. So the urgency to sell just wasn’t there anymore.

We are also going to spend the next couple of months building up our cash reserves through Sinking Funds and our Emergency Fund. We want a stronger buffer in the bank, particularly an emergency fund of around $18,000, which represents three months of spending. That gives us a level of comfort before Jonny steps away from his job.

And he is getting close to resigning. Once the cash reserves are where we want them, he’ll give plenty of notice, and in 2026, he will move on. At that point, his KiwiSaver contributions will also stop. Mine already have.

I’ve also made what feels like a slightly uncomfortable decision to slash our investing. Gulp. After prioritising investing over spending for so many years, pulling that back is not easy. We won’t stop entirely - we’ll still invest a very small amount each month - but that’s more of a behavioural choice than a mathematical one. It simply feels strange to go from doing something consistently for so long to not doing it at all. I will stop, just gimme a minute to adjust to this change!

This slightly strange middle ground

So now we enter this slightly odd middle ground.

We’re still earning an income, but we’re not working traditional jobs. Once Jonny resigns, we’ll both be in that space where it feels like we’re not really working, but we sort of are, as we continue to create The Happy Saver, something we both enjoy. Blogging and podcasting are unusual career choices; we have kind of fallen into them, but they seem to work for us. From the very beginning, the goal was to help people first, at no cost. I have always enjoyed helping and volunteering. Nothing has changed. We always said that if we earned money, it would be a bonus. Somehow, that bonus has grown into an income that now covers our annual expenses.

And those expenses include a full life: day-to-day living, travel, and supporting our daughter through university.

To sum up, our income covers all our expenses. Our investments are growing without additional capital. We are ‘safe’ to stop investing.

The safety net (because of course there is one)

It’s not a YOLO decision, either. We have a backup plan for our backup plan. We’ll have a fully funded emergency account, our sinking funds will be in good shape, and if needed, we can always sell a small slice of our investments, as we have happily done in the past. Realistically, I don’t expect that to be necessary in the short term, and we’ll likely continue to pick up bits of extra income here and there, as we always have.

We enjoy having a home that we can easily leave

There are still a few things to sort out around the house. We had already started doing maintenance to get it ready for sale (hence Jonny falling off a ladder and breaking his pelvis and arm, which was not part of the plan), and that work will continue. Houses always need attention, which is probably the biggest downside of owning one. But we’re approaching it differently now, with more job-sharing between us and a willingness to pay for help when we need it.

Ultimately, we want a ‘lock and leave’ home, where we can head away at short notice and know everything will be fine (including the cat). That’s what we’re working towards.

Why this finally feels right

What surprised me most was how quickly things shifted once we decided to stay. The moment we said, “we’re keeping the house,” I felt a weight lift. I stopped looking at everything through the lens of “what would a buyer want?” and started seeing our home for what it is again - a place we genuinely like.

Gosh, so freeing.

For a long time, the plan that made the most sense on paper was to sell, invest more, and then retire Jonny. And logically, that still stacks up. But there’s something to be said for trusting the math of investing enough to find a middle ground where we think, for now, we can have the best of both worlds: the freedom for Jonny to quit work, the freedom to keep this house, and the financial freedom to enjoy spending money on the life we want.

For us, it’s relatively simple now.

We’re keeping the house

We’ve slashed our investing

Our income covers our lives

Our investments continue to grow in the background

And when the work income eventually stops, those investments will be there to take over.

Personal finances are just that, personal. We have so many options and opportunities, all of them good, which makes it hard to navigate a path. But for us, for now, this feels like a good solution.